« Return to 2017 August Managing Change Issue Index

Don’t let claims follow you into retirement

Lawyers often approach retirement feeling good about their legacy. Whether you devoted your efforts to crafting airtight contracts, supported clients as they worked toward mediated settlements, or stood up for the rights of those who needed you, you’re entitled to feel proud of your accomplishments. Looking back, however, may heighten your awareness of just how many decisions your work required you to make. How likely is it that 100 per cent of your choices were correct?

While it’s impossible to be certain whether you’ll be “home free” from a claims perspective after you retire, you can take steps to limit the potential for claims to derail your financial plans. This article provides an overview of insurance considerations for lawyers making the transition out of traditional practice. (This article is based on a more detailed paper Leaving practice: Insurance considerations prepared by Victoria Crewe-Nelson, AVP Underwriting at LawPRO, for presentation at the Hamilton Law Association’s 15th Annual Estates & Trusts Seminar on February 9, 2017.)

What’s your risk?

Your exposure to claims in retirement depends on a range of factors, the most important of which are the nature of your work while practising and your professional activities after retirement.

How your pre-retirement practice area impacts your exposure

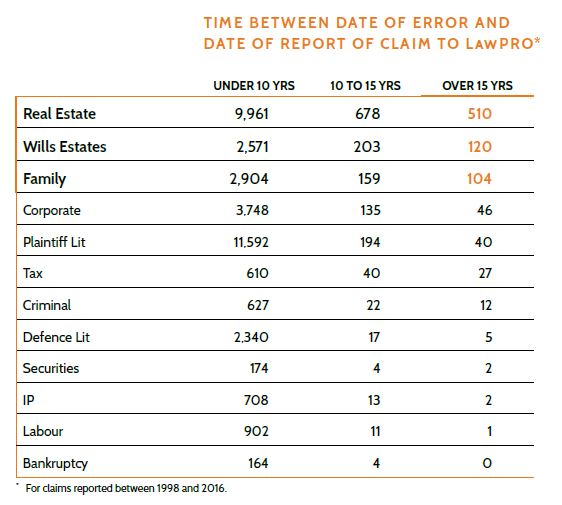

Just as malpractice risk varies based on area of practice during active practice, it also varies in retirement. While some types of claims are discovered shortly after services are rendered, others take years to develop. Examples of long-tail exposure activities include real estate work, and the preparation of domestic contracts and wills. LawPRO’s experience with claims reveals the following information about how long claims take to develop:

Whether a claim will come back to haunt you in retirement depends on the application of limitation periods, which can be affected by issues like delayed discoverability and whether potential claimants have been under a disability during the intervening years.

Protecting yourself financially may require that you increase the run-off coverage available to you – even if you practised with a firm that carried excess insurance (more on this below).

While you are thinking about your claims exposure, you may also want to review your history of providing services that fall outside the ambit of your LAWPRO coverage – for example, acting as a director on a client’s board of directors, acting as an estate trustee, managing private mortgages, or serving as an intellectual property agent. Will you be continuing in these capacities after retirement? If so, you may want to consider obtaining other categories of insurance, such as directors’ and officers’ insurance (“D&O”) or executors’ insurance.

What, exactly, do you mean by “retirement”?

The other important factor to consider when assessing your risk is whether or not you will continue with any professional activities that could attract liability after you officially “retire.”

For many lawyers, retirement is less a date than it is a process. Transitioning out of practice may mean declining new retainers but continuing to work on existing files as you transfer matters to other lawyers, reducing the hours worked over time. How you choose to transition out of practice will have an impact on your insurance requirements and options, especially if you decide to keep a foot in the door by acting as a trustee, by mentoring younger lawyers, or by providing pro bono services.

What are your coverage options?

For a few lawyers who maintain a significant involvement with the law, it will be necessary to keep the regular LAWPRO program coverage in place even in retirement. If you continue to provide legal services in any capacity – including as a mediator, arbitrator, trustee, or attorney, new risks for claims will continue to arise, and you may have to maintain practice coverage despite the services only being provided on a very occasional basis.

For most retired lawyers, however, retirement means new options.

Coverage for part-time practice

Lawyers making a gradual transition out of practice may be eligible for the part-time practice option. To qualify a lawyer must, in both the current and previous fiscal year, restrict his or her work to 20 hours per week on average for each week actually worked, and 750 hours per year. Maximum annual billings must not exceed $75,000 per year. The lawyer must also have not had a claim reported under the mandatory insurance program with a repair and/or indemnity payment in the last five years. If eligible, the lawyer will have the same level of coverage as is available under the base program, while paying 50 per cent of the annual premium.

Considering a retirement test-drive?

A few lawyers may need – or choose – to step away from practice temporarily before they are ready to retire. While some such leaves are prompted by the illness of a family member, others are taken to make time to study, to pursue a personal project, or even to sail around the world. As long as the lawyer has the intention to return to practice after the proposed leave of absence, he or she can apply under exemption C of the Primary Professional Liability Program to maintain the coverage limits offered to practising lawyers ($1 million per claim/$2 million in the aggregate) for up to five years for a leave taken for reasons of family or illness, or up to two years for other reasons. (This exemption is not available to lawyers who have taken alternative employment or who have been required to cease practice by the Law Society.)

Run-off coverage

Once a lawyer is truly out of the private practice of law, he or she enjoys the protection of LAWPRO’s standard run-off coverage without having to pay annual premiums (for full details of run-off coverage, see Endorsement No. 9 of your LawPRO policy). This coverage, though reassuring, is basic: it covers up to $250,000 in claims in the aggregate. Unlike the standard program mandated by the Law Society, the coverage limits are not refreshed annually – once claims hit the $250,000 threshold, there is no further coverage.

A limit of $250,000 will be adequate for certain lawyers, including those who were never in private practice and who may only be worried about “phantom client” scenarios (instances in which individuals may have misinterpreted casual conversations or presentations as legal advice). However, the majority of lawyers will need to think hard about the potential for the basic run-off coverage to be wiped out by a single large claim. The number of claims handled by LAWPRO with a value of over $100,000 has risen sharply in the past ten years; and one out of every 40 claims exceeds $250,000. When you consider the current pace of growth in the value of residential properties in Ontario, it becomes clear that any area of practice that involves disputes over property – including real estate, family law, and wills – has the potential to generate a high-value claim.

Run-off coverage buy-up

Retiring lawyers eager to protect their retirement savings can apply to “buy-up” their run-off coverage to a higher limit for a term of between two and five years (a further term can be applied for afterwards, if necessary). The level of run-off coverage can be increased to $500,000 per claim/in the aggregate, or $1 million per claim/$2 million in the aggregate. This coverage is individually underwritten, so the cost of the buy-up premium varies according to risk.

Run-off coverage generally applies to the same activities that were once covered by the lawyer’s previous LAWPRO policy coverage. However, to reflect the fact that many lawyers are named to act as estate trustees or attorneys for property for non-family members and that these obligations extend into retirement, lawyers can apply under exemption rule H to have increased run-off coverage apply to post-retirement services as estate trustee, inter vivos trustee or attorney for property, provided that the relevant appointment(s) were made while the lawyer was in active practice.

Don’t assume a former firm’s excess coverage will take care of it

Lawyers sometimes make the error of believing that an excess coverage policy held by the firm for which they once worked will make run-off buy-up unnecessary. However, excess coverage typically only “kicks in” above a certain threshold (usually the $1 million per claim limit provided by the Law Society mandatory program). This means that the lawyer will be responsible for the $750,000 gap between his or her run-off coverage and the firm’s excess coverage. Another caveat – reliance on one’s firm’s excess coverage presumes that the firm will remain in business, or will maintain the coverage for a sufficient period if it does dissolve.

What about claims against a lawyer’s estate?

Run-off buy-up can also be purchased by a lawyer’s estate. This can be especially important where a lawyer dies unexpectedly while in active practice – before he or she has taken steps to wind down and /or transfer files. See the article “A critical issue often overlooked in lawyers’ estate planning” below for an example. In fact, few lawyers instruct their spouses or estate trustees to purchase increased run-off insurance after they die. This risks leaving the estate and its beneficiaries vulnerable to claims.

For solo and small firm lawyers, limiting the claims exposure of your estate also means having a contingency plan ready in case, whether due to death, illness, or any other cause, you can’t continue acting for clients. The Law Society of Upper Canada has created the Contingency Planning Guide for Lawyers, a free resource to guide the creation of a contingency plan. At the heart of the plan will be the selection of a replacement lawyer who can take over the practice, avoiding prejudice to clients and related claims against the planning lawyer or his or her estate.

An effective plan depends on having a discussion with the replacement lawyer about a number of key issues. These include: whether the practice should be wound up or preserved for sale, compensation for the replacement lawyer, making arrangements for the replacement lawyer’s access to trust and general accounts, creation of a power of attorney to support the transition, and the appointment of the replacement lawyer as estate trustee for the planning lawyer’s practice.

Relieving worry about post-retirement mentoring and pro bono activities

Mentoring new lawyers is popular among retired lawyers seeking to retain a connection with the law. In recognition of the real value that experienced mentors can provide to new members of the profession, LAWPRO has taken steps to reduce aspiring mentors’ worries about liability. LAWPRO’s standard run-off coverage of $250,000 in the aggregate applies to claims against a retired lawyer arising out of a mentoring relationship, provided that:

- The mentor and mentee agree to a formal mentoring relationship, as evidenced by a written document of some kind;

- The mentor has no contact with the mentee’s client that would create a solicitor-client relationship; and

- The mentee understands that the mentee is responsible for individually and independently being satisfied of the soundness of any suggestions, recommendations or advice-like comments made by the mentor.

What about pro bono practice?

While LAWPRO does not generally cover the performance of legal services by lawyers on exemption (including retired lawyers), there is an exception for those lawyers who provide professional services through LAWPRO-approved pro bono programs associated with Pro Bono Ontario (PBO). LAWPRO’s standard run-off coverage covers work done for these programs even after the lawyer has gone on exemption. No deductible applies in the event a claim is made against the lawyer for legal services provided through approved PBO programs. Lawyers wishing to provide services for a not-for-profit organization that isn’t associated with PBO can maintain their exemption by applying to LawPRO and getting pre-approved. However, in these circumstances LawPRO’s standard run-off coverage will not cover the legal services provided, and in the absence of an indemnity agreement or insurance coverage being arranged by the organization, the lawyer may have exposure in the event of a claim.

Keep us in the loop

To ensure that you have the coverage you need and that you are kept aware of policy changes that might affect you, it’s important that even after retirement you inform us of changes to your contact information (address, phone number, and email). You can also get in touch with us to ask questions about the coverage status of professional activities you’re proposing to undertake. LawPRO’s Customer Service department can be reached by phone at 416-598-5899 or 1-800-410-1013, or by email at [email protected]

Counting on the ultimate limitation period?

As most lawyers know, section 15 of the Limitations Act, 2002 (the Act) sets a 15-year ultimate limitation period from the day the act or omission on which the claim is based took place, regardless of when the claim was discovered. Under the transition rules set out in s. 24, if a claim was not discovered before January 1, 2004, then January 1, 2004 is the deemed date the act or omission took place, and so January 1, 2019 would be the ultimate limitation period.

However, there are exceptions, some of which have the potential in rare circumstances to create liability for a lawyer beyond January 1, 2019. These include:

- The limitation period does not run during any time during which the person having the claim is under a disability and is not represented by a litigation guardian with relation to the claim (s. 15(4)(a));

- The limitation period does not run during any time during which the person having the claim is a minor and is not represented by a litigation guardian with relation to the claim (s.15(4)(b));

- The limitation period does not run for the period during which the defendant wilfully conceals the claim from the person who has it (s.15(4)(c)(i)); and

- The limitation period does not run during the period during which the defendant misleads the person having the claim about the appropriateness of bringing an action (s.15(4)(c)(ii)).

Another type of exposure that may survive beyond the ultimate 15-year limitation period would be a claim for contribution and indemnity, as anticipated by s. 18(1) of the Act.

As a result, lawyers cannot safely assume that, as of January 2, 2019 they will be free from liability flowing from all legal work done prior to January 2, 2004.

A critical issue often overlooked in lawyers’ estate planning

When a lawyer passes away while still in active private practice, LawPRO’s run-off coverage kicks in. While standard run-off may be enough coverage for lawyers who have been retired for several years (since potential claims will have had time to develop), it may not be sufficient for a lawyer who was practising full-time at the time of his or her death.

A real example from our files demonstrates what can happen. Carol’s husband, a lawyer, passed away in 2010. When Carol reported her husband’s death to LawPRO customer service, the program coordinator who responded advised her of the option to purchase increased run-off insurance above the standard $250,000 limit set out in the policy. Carol opted to increase the run-off coverage insurance to $1 million. Two years later, Carol was served with a Statement of Claim in relation to legal services performed by her husband. Damages in that litigation may well reach $1 million. LawPRO is defending the action.

Subject to exclusions or other policy provisions, the LawPRO policy provides coverage limited to $1,000,000 per claim and is subject to an aggregate limit of $2,000,000 per policy period (i.e., per year.). However, upon retirement or death, standard run-off coverage is limited to $250,000 in total, regardless of the number of claims made against the insured or the time period in which they are made. Given that we see claims reported, on average, two to three years after legal services have been provided (and nearly half of wills and estates claims take at least five years to develop), there is no question that a lawyer or the lawyer’s estate remains exposed to liability even after retirement or death. For many lawyers, $250,000 in coverage, inclusive of defence costs, will simply not be enough.

Unfortunately, few lawyers leave instructions for their spouse or other estate representative

to purchase increased run-off insurance after they die – thus leaving the estate with the total maximum coverage of $250,000 for all future claims against the lawyer. Consider the type of work you do: the subject matter of your litigation files, the transactions you have closed, the wills you have drafted. Would $250,000 be enough coverage? Unless your estate or next of kin purchases increased run-off insurance, your coverage will indeed be limited to the standard $250,000 run-off coverage outlined in Endorsement 9 of the policy. We highly recommend that you prepare instructions for your estate representative to ensure that run-off coverage is considered and the estate is adequately protected. For complete details of the Run-off Buy-up coverage offered by LawPRO, please visit lawpro.ca.