« Return to 2026 April - Year in Review 2025 Issue Index

Preparedness Above All

Most professional problems don’t begin dramatically. They start small: a missed detail, an unclear instruction, a process that breaks under pressure, a tool that introduces unintended risk, or changes in law and practice that are difficult to keep pace with. In that environment, lawyers need a professional liability insurer they can rely on.

Protecting insureds amid rising complexity and E&O costs

Our claims experience in 2025 reflects rising claim volumes and a profession operating within an increasingly demanding, evolving, and costly risk environment. The increases in 2025 continue a steady trend of higher claim numbers and costs. Despite these pressures, the claims team achieved record file closures, strong litigation outcomes, and the rigorous defence of matters lacking merit. The following analysis examines key claims trends in 2025, including a breakdown of costs, practice area, and cause of loss.

Growth in claims and costs

A total of 3,940 claims were reported in 2025, an increase of just over 5% from the prior year. The number of claims has been on a steady upward trend over the last three years.

Higher claim volumes resulted from continued claims activity in high-risk practice areas, the resumption of administrative dismissals following the lifting of pandemic-era pauses, and growth in complex and costly litigation and estates work. Growth in the number of practicing lawyers also increased overall claim volumes. As the volume of newly reported claims continued to climb, the number of open files increased by 4.1% in 2025.

Claims costs rose in 2025, with increases in both indemnity payments and legal fees and expenses. Total program costs increased by 8% to $102.6 million, compared to $95.4 million in the prior year. The increase in indemnity costs reflects larger settlement mounts, while higher legal fees were driven by more complex and longer-running litigation matters, including files that proceeded to trial, as well as an intentional effort to move files toward resolution.

At the same time, the Claims team achieved a record-high closure rate, closing 3,823 files, an increase of 4% over the prior year. This outcome reflects the combined impact of staffing planning made in recent years, continued improvements and adaptability to the policy administration and claims management platform, and a dedicated and concentrated effort by the Claims team.

Survey results showed that 98% of respondents reported satisfaction with the claims professionals who handled their matters.

Despite higher indemnity payments overall ($41.3M in 2024 to $46.6M in 2025), the majority of claims continued to resolve without indemnity payments. About 89% of closed claims had no indemnity paid, with over a third closing without any payment.

LAWPRO continued to defend insureds vigorously against claims lacking merit, achieving strong results in matters that proceeded to trial or were resolved through summary judgment.

Let’s dig deeper: Claims trends by area of law and cause of loss

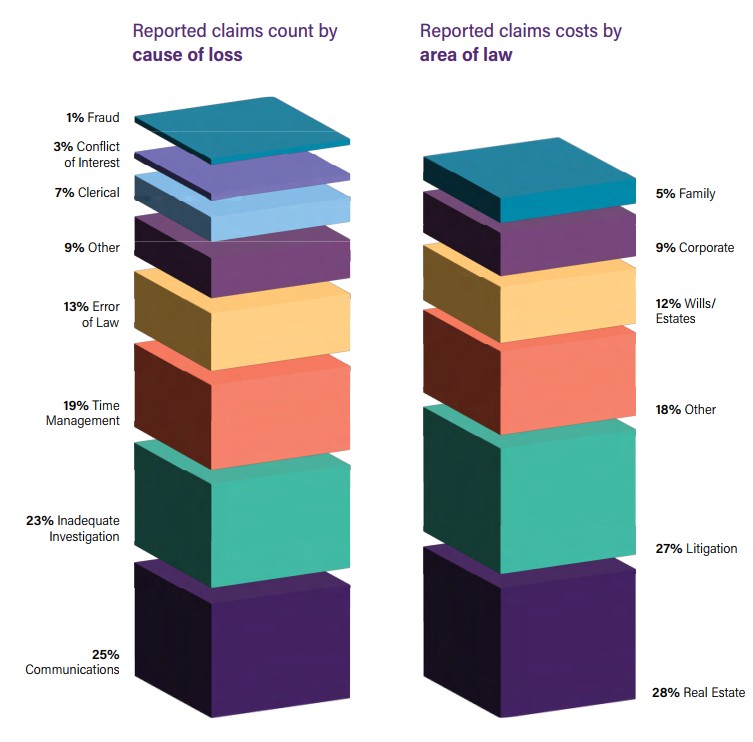

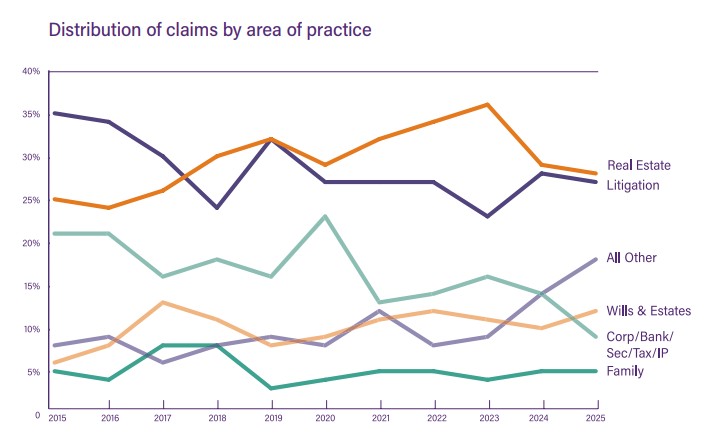

The distribution of claims by area of law in 2025 remained largely consistent with historical patterns. Real estate and litigation continued to account for the largest share of reported claims, together representing approximately half of all new matters. Across practice areas, claims continued to be driven primarily by practice managementrelated issues — often described as “human” errors — with inadequate investigation and communication failures as the leading causes of loss.

Practice areas: real estate, litigation, and the runner up

Real estate claims declined slightly in 2025 compared to 2024, reflecting reduced market activity. Nonetheless, real estate remains a leading source of claims, most commonly arising from communication breakdowns and failures to conduct adequate investigation.

Litigation claims increased year over year, in part due to the resumption of administrative dismissals for delay following the lifting of pandemic-related holds in May 2024. As courts returned to more stringent enforcement of procedural timelines, missed deadlines and related issues became a more prominent source of claims, with impacts continuing in 2025.

Wills and Estates related claims are a growing area of concern as the Ontario’s population ages and the number of deaths increase. Increasing estate values, beneficiary disputes, and greater complexity remain key contributing factors to wills and estate claims. There has also been an uptick in family law claims arising out of estate proceedings where the lawyer previously acted in connection with domestic contracts or other family law matters..

Building on trends observed in prior years, 2025 saw an uptick in claims reported in labour and employment, criminal, and construction law, with more gradual increases in immigration and administrative law.

Cause of loss

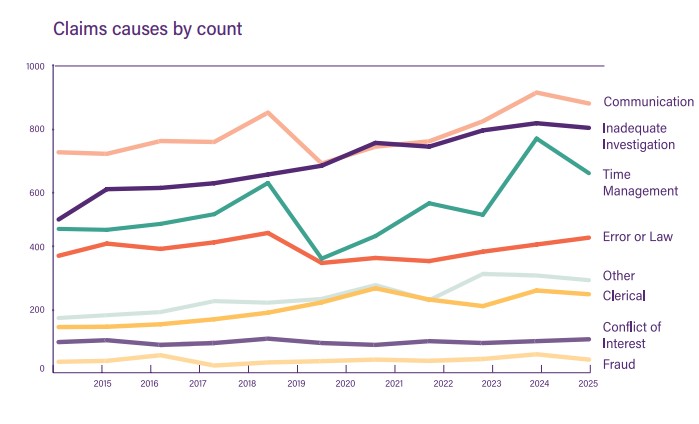

Analysis by cause of loss confirmed that inadequate investigation and communication errors remained the primary drivers of claims activity in 2025. These causes are closely associated with high-volume practice areas such as real estate and wills & estates, where matters often involve multiple parties, tight deadlines, and significant client reliance on legal advice and follow-through. Inadequate investigation typically reflects failures to fully identify or assess relevant facts, while communication errors often stem from unclear advice, unmanaged expectations, or poor documentation of communications and work completed.

Time management errors continued to be a significant contributor to claims, particularly in litigation practices. Stricter enforcement of procedural timelines after the pandemic, rising caseloads, shifting court processes, changes in legal representation, and more complex files all raise the risk of missed deadlines.

Error of law also increased in 2025, reflecting not only the growing complexity of legal matters but also the increasing difficulty of keeping pace with legislative changes, evolving case law, and shifting procedural requirements.

The chart below shows the number of fraud related claims as low but the cost is high, especially in certain practice areas such as real estate. Sophisticated schemes targeting lawyers and their clients persist, often resulting in losses in hundreds of thousands of dollars.

LAWPRO continues to monitor these trends closely to guide policy development, claims handling strategies, and develop practical risk management and education to support the profession.

Supporting and covering insureds

In 2025, LAWPRO delivered consistent customer service and robust underwriting, successfully adapting to changing conditions. LAWPRO maintained premium stability and steady financial performance amid volatile economic conditions while continuing to offer meaningful discounts, run-off protection, and optional coverage enhancements to lawyers. The Underwriting and Customer Service team supported insureds with their inquiries and maintained a steady response rate.

Premium

LAWPRO’s mandatory insurance premium continues to stand out. The base premium remained at $3,250 per lawyer in 2025, unchanged for nearly a decade and lower than it was in 2016, when the premium stood at $3,350. This long-term consistency is particularly notable at a time when costs have risen sharply across many industries and claims costs continue to trend upward. When adjusted for inflation, the base premium charged when LAWPRO was established in 1995 would exceed $11,600 today.

Discounts and options

The E&O Program includes a range of discounts and optional coverages designed to reflect how lawyers practice and how their needs change over time.

Discounts are available for new lawyers starting their careers, lawyers practicing part-time, and those working in restricted areas of practice. Such discounts help to align premiums more closely with actual risk. Lawyers who complete approved risk-management activities may also qualify for a Risk Management Credit, which provides up to $100 premium reduction in recognition of steps taken to reduce exposure and promote good practice habits.

Excess insurance

LAWPRO’s optional Excess insurance provides an additional layer of protection with insurance limits up to $19 million over the mandatory primary policy limit of $1 million. The program is designed primarily for small and mid-sized firms and sole practitioners, offering approximately 1700 law firms an accessible way to increase protection with a familiar professional insurer.

In 2025, the Excess program continued to demonstrate financial stability and modest year-over-year revenue growth. Adapting to changes in the profession, including an increase in sole practitioners retiring, the program placed greater emphasis on supporting insureds seeking higher excess limits the evolving risk profiles of their practices.

Title insurance – TitlePLUS

TitlePLUS is LAWPRO’s title insurance program and is the only wholly Canadian-owned title insurer in Canada. TitlePLUS includes legal services coverage for errors or omissions made by the lawyer for the entire transaction (excluding Quebec and Existing Owner policies), ensuring the LAWPRO E&O Policy remains unaffected.

In 2025, TitlePLUS successfully implemented significant mandatory anti-money laundering changes arising from new FINTRAC reporting obligations applicable to all title insurers. Required updates to documents, systems, and processes were implemented seamlessly, enabling TitlePLUS to continue issuing policies efficiently despite across-the-board changes to real estate practice workflows.

Delivering committed support

LAWPRO’s Underwriting & Customer Service (UCS) team is the primary point of contact for lawyers seeking support with their insurance coverage throughout the year and during the annual renewal process. The team is responsible for policy drafting, maintaining accurate policy records, processing applications and changes, underwriting optional coverages, supporting premium collection, and answering questions about coverage, billing, program requirements, and access to My LAWPRO portal.

In 2025, the team supported approximately 33,000 insured lawyers and handled more than 36,000 calls, most commonly related to coverage and billing matters. During renewal, the team assisted lawyers and with filings and access issues to help ensure coverage is confirmed and policy documents are issued, resulting in a successful renewal process to kick start 2026.